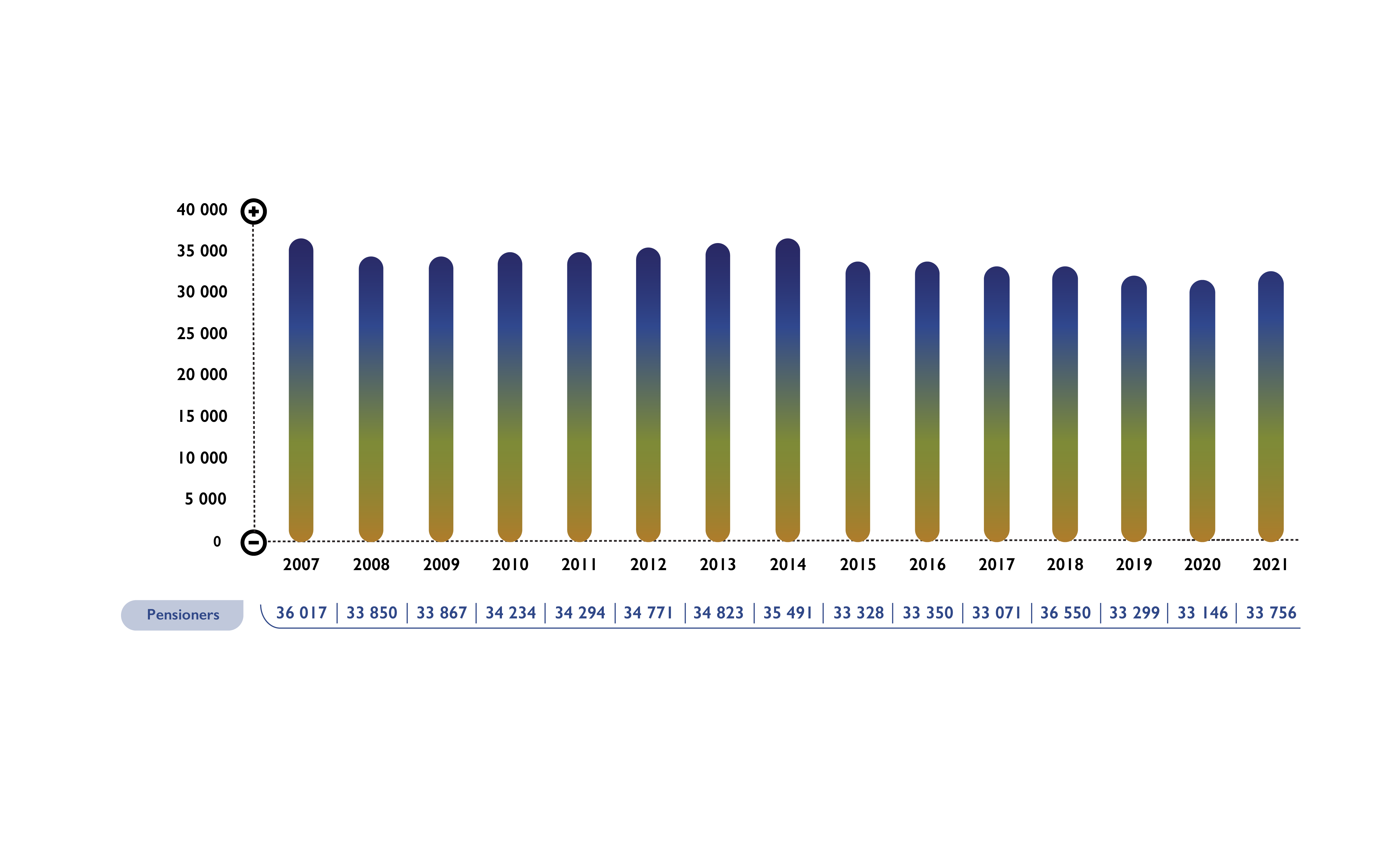

Pensioners of the EPPF are former in-service members who retire from the service of the employer OR deferred members (over the age of 55) who elect to start receiving a monthly pension from the EPPF.

Read morePensioners of the EPPF are former in-service members who retire from the service of the employer OR deferred members (over the age of 55) who elect to start receiving a monthly pension from the EPPF.

In Remembrance

Title

First Names

Surname

Age

Date of deathD.O.D

MRS

WILHELMINA MAGDALENA

ALEXANDER

81

10/29/2023

MRS

ANNELI RACHELE

APPELGRYN

58

11/29/2023

Mrs

MARTHA

APRIL

61

11/1/2023

MRS

NOSAKHELE

BANGAZILE

98

11/2/2023

MRS

RITA ANNE

BARNES

91

11/22/2023

MR

RONALD CLAUDE

BATTEN

87

10/10/2023

MRS

WILHELMINA ALEXANDER

BEHR

85

10/13/2023

MNR

SYDNEY GODFREY

BESTER

79

11/17/2023

MRS

NONTSIKELELO

BLAKFESI

49

12/3/2023

MR

MARK ROBERT BAXTER

BLEAKLEY

88

11/20/2023

MR

LESLIE GRAHAM

BOOTH

75

11/29/2023

MNR

DAVID JOHANNES

BOTES

79

10/29/2023

MNR

JOHANNES JACOBUS

BOTHA

84

11/6/2023

MRS

EMMARENTIA PETRONELLA

BOTHA

82

11/28/2023

Mr

RETIEF

BOTHA

78

11/19/2023

MRS

GLORIA ANNA

BOUCHET

83

11/24/2023

MNR

JOHANNES MATHYS

BRITS

83

10/8/2023

MRS

IONA ANGELINE BEATRICE

BROWN

81

11/24/2023

MR

JOSE GONSALVES

CHADINHA

88

11/12/2023

MRS

MAUTATA ANNAH

CHATSANA

79

11/23/2023

MRS

LETTIE MAMAHLATSI

CHEGO

61

10/15/2023

MRS

WILHELMINA FARQUHAR

CHISHOLM

93

10/10/2023

Mrs

JEAN

CLIFF

88

11/3/2023

MRS

SYLVIA ANN

COATES

89

10/22/2023

PETRONELLA CATHARINA ALETTA

COERTZE

69

11/17/2023

MRS

MARIA ELIZABETH

COETZEE

87

10/18/2023

MNR

JAMES IGNATIUS

COETZEE

85

11/27/2023

Mr

ANDRE LEON

COLEMAN

66

11/6/2023

MR

DESMOND ARCHIBALD

DAMSTER

92

10/26/2023

MRS

MAGARETHA ELORINA

DE BEER

92

11/11/2023

Ms

ANNE MARIE

DE BRUYN

54

11/6/2023

MEV

JANETTE CLASINA

DE NECKER

67

10/2/2023

MR

CHRISTIAAN PETRUS ADOLF

DIEDERICKS

81

11/12/2023

MRS

PHOGCILE

DLAMINI

93

11/15/2023

Mr

ALLAN DENVER

DOLIVEIRA

63

10/21/2023

MRS

HESTER CECILIA SMITH

DU PLOOY

84

11/28/2023

MNR

Johannes Lodewikus

DU PREEZ

77

10/20/2023

Mr

NKOSIYETHU

DUMA

66

11/7/2023

MR

MADODA BISHOP

DYANTYI

74

11/7/2023

MR

JOHN GORDON

ELLISON

93

11/11/2023

MNR

ALBERTUS ABEL

ERASMUS

79

12/4/2023

MR

PETRUS PAULUS

ERASMUS

76

10/1/2023

MR

JOHN HENRY NAUDE

FARRELL

74

11/24/2023

Mrs

MARIA CATHERINA

FOURIE

58

10/10/2023

MRS

YVONNE AMY

FOWLER

91

10/18/2023

MRS

MARIE

GENIS

80

11/15/2023

Mrs

NONTOAZITHETHWA RIENED

GIGABA

69

11/10/2023

MNR

NICOLAAS CHRISJAN PIETERSE

GOUWS

74

11/13/2023

MNR

CHRISTIAAN MAURITZ

GROBBELAAR

82

10/19/2023

MNR

HENDRIK FREDERIK

GROBLER

86

10/26/2023

Mr

PIETER ALBERTUS

GROBLER

66

11/30/2023

Mrs

ELIZABETH JACOBA

GROVE

79

12/5/2023

MRS

NOMPUMELELO ELLA

GUSHA

89

10/15/2023

MNR

MNWANA ROGERS

GWINTSA

85

10/4/2023

MRS

MAVIS NOMATHAMSANQA

HADABE

64

12/4/2023

MNR

HERMAN GERARD

HANEKAMP

71

11/27/2023

MRS

NELLY MARGARET EILEEN

HEIDTMANN

79

10/13/2023

Mrs

EILEEN MARGARET

HOLDER

80

11/20/2023

Mrs

LYN

HOPKINS

83

10/3/2023

MR

THELMAN FRANCOIS

HORN

75

10/19/2023

MR

GEOFFREY MORRIS

JANES

96

10/28/2023

RICHARD STEVEN

JARDINE

94

11/17/2023

MR

XWASHU

JIBILIKILE

88

10/6/2023

Mr

PETRUS JACOBUS

JOUBERT

66

11/3/2023

ANNA MAGRIETA

KATZKE

81

12/7/2023

MRS

NONAYILESE

KENKEBE

69

11/2/2023

SYLVASIA NONTLANTLA

KHAMBULA

71

10/27/2023

MRS

NCINELENI MARIA

KHANYILE

73

12/4/2023

MR

FRANCES KHABANE

KHOTSO

72

11/6/2023

MRS

JULIET ZIBUYILE

KHUMALO

65

11/6/2023

Mrs

MURIEL ANSIE

KINSELA

84

10/24/2023

MNR

GERT

KLEYNHANS

80

12/7/2023

MR

QATIKO

KOTI

72

11/20/2023

MRS

MARIE MAGDALENA

LANGSTON

87

11/17/2023

Ms

GONKE TESSA HERMI

LANTERME

77

10/28/2023

MR

MARVEL GEROME

LE ROUX

65

10/23/2023

MRS

BAOETSE ONICA

LEBUSO

83

11/26/2023

MR

MONYAKE ABRAMHAM

LECHOO

78

10/23/2023

MR

NEPHTALY MABOE

LENKO

72

11/9/2023

ANNETTE

LERM

78

10/4/2023

MRS

AMELIA MAKHATISO

LETLOFA

83

10/28/2023

MR

NTSHAVHENI JACKSON

LIPHADZI

73

11/28/2023

MRS

PHOPHI AZWIHANGWISI

LIVHALANI

73

10/4/2023

MR

ZWELIBANZI AARON

MABANGULA

76

11/16/2023

MR

SOLLY PHILLIP

MABENA

70

11/27/2023

Mr

THEBE JEREMIAH

MABUNGU

66

11/6/2023

MR

NKULUMO JAMES

MABUZA

64

10/25/2023

Mrs

NOLASI

MACALA

77

12/5/2023

MRS

LESEDI ELIZA

MADUPE

73

11/28/2023

Mrs

NOWONGILE VICTORIA

MAGODLA

80

12/6/2023

MRS

THANDI MARTHA

MAGOLEGO

63

10/5/2023

Mrs

BETTY

MAHLANGU

74

11/29/2023

MR

JEREMIAH KLEINBOOI

MAHLANGU

72

11/15/2023

Mr

MAKOMANE SAMUEL

MAHLOKO

69

10/27/2023

MISS

ANNA JACOMINA

MAKKINK

72

11/3/2023

MRS

RAMASHIGO MARIA

MAKUA

80

11/4/2023

MR

MATHANGANA ISIAH

MALIBA

98

11/2/2023

KWARI HESSIE

MALINGA

81

11/25/2023

MR

NGUSHA JAMESON

MALINGA

76

11/13/2023

MRS

DINA MASHIANYANE

MAMOSHI

59

10/9/2023

Mr

PAULOS TEMBA

MANANA

79

11/3/2023

MRS

NONKOHLAMTU MAGGIE

MANGALISO

70

11/26/2023

MRS

MARIA PETARENELLA

MARKHAM

96

10/10/2023

MRS

MANTSHIUWA JEMINA

MASEKO

60

10/16/2023

Mr

PIET

MASHILOANE

69

10/24/2023

MRS

POPIE BETTIE

MASHILOANE

65

11/12/2023

MR

MZIMBILI ESSAU

MASHININI

100

11/9/2023

MR

MVINJELWA FATMAN

MASOMBUKA

78

11/28/2023

MR

MDAU SOLOMON

MATHABELA

75

10/15/2023

MR

TUZELELE JOHANNES

MATOMANE

74

10/4/2023

MR

KALOSHI MORRIS

MAZWI

77

10/11/2023

Mr

THEMBINKOSI WILLIAM

MBALI

61

10/10/2023

Mrs

ESTHER MAKHOSAZANA

MBHELE

67

10/9/2023

MR

MAGEQE MOSES

MBINGO

70

10/2/2023

MRS

MARJORIE MOFFATT

MCNAUGHTON

89

11/12/2023

Mr

MBUZENI

MDLETSHE

73

10/8/2023

MRS

ALICE MARTHA

MDLULI

71

10/14/2023

Mr

Dennis Alexander

MEIKLE-BRAES

63

11/26/2023

Mr

GEORG PHILLIPUS

MEINTJES

96

11/25/2023

MRS

NOMVUYO SYLVIA

MENE

83

10/15/2023

MR

MADLIMALI ABEL

MHLANGA

86

11/24/2023

MNR

JOHN HENRY

MITCHELL

81

11/26/2023

MR

MTSHIKOLO ERNEST

MIYA

75

10/22/2023

MR

JIKAJIKA

MKENKE

74

12/4/2023

MR

SATAN

MKHATSHWA

84

11/17/2023

MRS

SALAZE

MKHIZE

85

10/6/2023

Mr

GULANA ALBERT

MLAMBO

77

10/18/2023

Mr

BEKIE SOLOMON

MNGOMEZULU

67

10/5/2023

ZODWA ELSIE

MNISI

46

11/14/2023

Mrs

MIENA

MNYAKA

78

10/15/2023

MISS

REBECCA

MOAGI

76

10/11/2023

MR

ELIAS DUGMORE MOLEFI

MOKATSANE

70

11/29/2023

MR

HOLOANE MARITENS

MOKOANA

86

11/2/2023

MR

SETIMELA WILSON

MOLA

97

11/2/2023

MMAKAPA GWENNIAH

MOLALE

76

10/6/2023

Mrs

MIRIAM

MOLLER

78

11/16/2023

MRS

RAISIBE MAPOSA

MOLOTO

80

10/8/2023

Mrs

LYNETTE BAXTER

MOMBERG

68

11/19/2023

MR

DIRKIE ANDRE

MOOLMAN

65

10/8/2023

MR

RICHARD WILLIAM

MORRIS

89

10/31/2023

MEV

LIDIA CATHRINA

MOSES

60

10/2/2023

MRS

EMILY

MOSIA

86

11/11/2023

ROBERT WILLIAM

MOSTERT

64

11/24/2023

Mrs

NANKI NANCY

MOTIANG

68

11/20/2023

MRS

THENGANI JOYCE

MSEZANE

83

12/5/2023

MZIMI FLORENCE

MSHIBE

69

10/12/2023

MR

JABULANI ENOCH

MSIBI

71

10/19/2023

Mrs

BUSANGANI NINA

MSIBI

62

12/1/2023

MRS

LIMAKATSO PAULINA

MSIMANGA

78

11/27/2023

MRS

SEBENZILE

MSOMI

78

10/31/2023

MRS

MPATSHASI SOPHIE

MTHOMBENI

87

11/16/2023

Mr

MANDLA UTRICK

MTHOMBENI

77

11/4/2023

MRS

JULIA

MTSHALI

106

12/4/2023

MRS

TSHENGISILE MITCHEL

MTSHALI

62

10/30/2023

Mr

SONOSAKHE

MTUNGWA

68

10/28/2023

MRS

ANNA MAGDALENA

MUNRO

89

10/14/2023

MNR

WILLEM ANDRIES

NAUDE

89

10/21/2023

MR

SIYANDA BRUCE

NCAMISO

44

11/11/2023

Mrs

MAKANA ANNAH

NDHLOVU

65

10/21/2023

MR

WELE HENRY

NDWALAZA

76

10/25/2023

Mr

NALEDZANI ROBERT

NEMANAME

67

12/3/2023

MRS

KHANYISIWE LELE

NENE

87

10/7/2023

Mr

GEORGE

NENE

64

11/5/2023

MRS

MAMBILA

NGOBENI

96

11/6/2023

MRS

WENDY BETHUSILE

NGOBENI

59

10/4/2023

MR

ZONDI ARON

NGOMA

70

10/11/2023

Mr

BUSANI JAN

NGWENYA

61

11/10/2023

MRS

HLEZIPHI THOMO

NGWENYA

61

10/25/2023

NULL

ZIBIZANI

NHLENGETHWA

85

10/12/2023

MRS

CHRISTINA CATHARINA FREDERIKA

NICHOLAS

86

10/29/2023

NULL

CHRISTINA CATHERINE FREDERIKA

NICHOLAS

86

10/29/2023

MR

GIJA SIZE

NKALA

87

12/2/2023

Mrs

NCANE MARTHA

NKOSI

77

11/19/2023

MR

SIBONGISENI THOMAS

NOMBAMBO

77

10/30/2023

MR

NGIZI

NOTA

86

10/3/2023

MRS

LYDIA BELINA

NTANDANA

67

10/22/2023

MRS

ALINA MATSOELA

NTSALA

76

12/1/2023

Mrs

MAVIS THEMBISILE

NTSHINGILA

71

11/24/2023

MR

SAMUEL PETRUS

NTULI

87

11/29/2023

MRS

BATHABILE PRETTY

NYAMBI

44

11/26/2023

Mrs

DWALILE JULIA

NYONI

72

11/14/2023

MRS

WILHEMIENA

OLIFANT

71

11/23/2023

Mrs

MARGRIETHA ELIZABETH

PALMER

80

11/23/2023

Mrs

MARIE

PAULSE

80

10/2/2023

MRS

MASEILE ELISA

PHOLOANYANE

82

10/10/2023

MRS

DAPHNE HILDA

PIETERSE

80

11/22/2023

Mr

NICOLAAS ALBERTUS PETRUS

POOL

78

11/14/2023

Mrs

CATHARINA HESTER JOHANNA

POTGIETER

76

10/17/2023

MEV

PETRONELLA JACOBA

PRETORIUS

73

10/11/2023

MR

MANDLA

QOZA

72

11/6/2023

Mr

MATOME

RAKGAKOLE

67

10/19/2023

MEV

ESTER

REYNECKE

87

11/7/2023

MRS

HELEN

ROBBINS

99

10/13/2023

MR

RAYMOND GORDON

ROBINSON

74

10/2/2023

Mr

MESHACK

SAKATI

61

10/6/2023

MNR

HENDRIK LOUIS

SCOTT

82

10/2/2023

MR

MSHUSHISI WILTON

SHEKWA

71

10/15/2023

MRS

MAGRIETA MARTHA

SIBANYONI

77

12/4/2023

Mr

MBULAHENI CARLSON

SIBIDE

77

10/15/2023

MRS

NTOMBIKAYISE LINAH

SIFUNDA

75

10/25/2023

MRS

TYEKWA EVELINA

SILINDA

83

10/6/2023

MRS

ASSA ELLINAH

SIMANGO

83

11/21/2023

MRS

SETHULELE ESTER

SIMELANE

81

11/3/2023

MRS

NTOMBEZISHOYO EUNICE

SIMELANE

71

11/12/2023

MRS

SAMARIA HLEZIPHI

SINDANE

69

10/29/2023

Mrs

GABOITSIWE SUZANNE

SISING

87

11/25/2023

MRS

MARIA TSHABISANG

SITHOLE

88

10/5/2023

MRS

REMAKETSE IMELDA

SIYALI

64

10/15/2023

MR

STEFANUS DE CLEREQ

SMAL

101

12/5/2023

MRS

CORNELIA JOHANNA

SMAL

93

11/13/2023

MAUREEN FAY

SMITH

94

11/23/2023

MR

ERIC LEONARD

SMITH

88

10/28/2023

Mr

JOSEPH KENNETH

SMITH

80

11/11/2023

MR

JOHN ARMSTRONG

SMITH

78

10/31/2023

MNR

CORNELIS ALWYN

SMITH

71

10/5/2023

Mr

DAVID BENJAMIN

SNYMAN

76

10/20/2023

MR

DAVID BENJAMIN

SNYMAN

76

10/20/2023

MRS

PIETRO MAGDALENA

STRYDOM

70

11/21/2023

MNR

FREDERIK JOHANNES JACOBUS

SWIEGERS

69

10/2/2023

MR

PHINEAS PHUTI

TAU

73

11/16/2023

Mr

SENYATJA JONAS

TEMA

73

10/8/2023

Mr

NICOLAAS JACOBUS

TERBLANCHE

73

10/21/2023

MNR

JOCOBUS JOHANNES

TERBLANCHE

65

11/26/2023

Mr

JOSEPH MOSOTHO

THAMAE

75

11/9/2023

Mr

FLORIS PETRUS

THIRION

64

11/18/2023

MR

DANIEL JACOBUS

TIEMIE

71

12/1/2023

MR

MABANDLA FRANS

TLEMA

78

11/12/2023

MR

MPOYAN JOHN

TSEHLA

94

11/8/2023

MR

ANDREW

TWYFORD

58

11/25/2023

Mrs

MARIA MAGDALENA

UYS

80

10/29/2023

MRS

SUSARAH CORNELIA

VAN EMMENIS

74

11/4/2023

MEV.

ANNA CATHARINA DOROTHEA

VAN NIEKERK

82

11/3/2023

MR

FREDERICK GORDON

VAN NIEKERK

72

10/21/2023

SUSANNA MAGDELENA

VAN OORDT

78

11/21/2023

Mrs

BARBARA ANN

VAN SCHOOR

85

10/21/2023

MNR

JOHAN JURGENS

VAN ZYL

90

10/25/2023

MRS

JOHANNA MAGDALEEN

VAN ZYL

70

11/14/2023

Mr

CHRISTIAAN RUDOLF

VENTER

70

11/28/2023

MEV

ADRIANA CECILIA

VERMAAK

84

11/30/2023

MEV

MARTHA FRANCINA MARIA

VISAGIE

91

10/27/2023

MEV

ANNA MAGRIETA

WATERBOER

81

10/5/2023

Mrs

ANNA SUSANNA MAGDELENA

WILKEN

71

10/29/2023

NOMALAWU

XOBISO

72

10/31/2023

Mrs

NOMATHEMBA IVY

ZAMANI

71

11/8/2023

MRS

EDITH KHOTATSO

ZIMBA

65

10/20/2023

MR

SAMUEL HUMPHREY

ZITHA

64

10/12/2023

MR

SITHEMBISO MORRIS

ZOZO

69

11/20/2023

MR

DUMISANI ABRAHAM

ZULU

63

11/26/2023

MRS

KHUBA JOHANNA

ZWANE

83

11/25/2023

Pensioners of the EPPF are former in-service members who retire from the service of the employer and draw a pension from the EPPF.

Children over the age of 21 (major children) or any other beneficiaries/nominees of a death benefit can renounce their benefit by completing the Renunciation of Benefits Claim Form. Click here to download the form and submit to the Fund.

Spouses of deceased members and pensioners of the EPPF, as well as qualifying children in receipt of a pension are beneficiaries of the EPPF.

Normal Retirement

The EPPF’s compulsory retirement age is 65 years. However, in-service members may retire early from age 63 without penalties, subject to the employer’s conditions of service. The benefit is based on 2.17% of the in-service member’s annual average pensionable salary over the last year before retirement, for each year of pensionable service.

Early Retirement

An in-service member may retire early after reaching age 55 years. The benefit is a pension calculated in terms of a pension formula, reduced by the penalty factor of 3.9% per year for each year before age 63 years.

Ill-health retirement

An in-service member may retire at any age as a result of ill-health, provided that the Board of Trustees approves a recommendation by the EPPF Medical Panel in this regard. The benefit is calculated by making provision for a pension based on the in-service member’s pensionable salary and pensionable service accrued up to the actual retirement date plus 75% of the service that would have been completed by the in-service member from that date to the pensionable age.

Death after retirement

On the death of a pensioner, a lump sum equal to R3000 is paid to the surviving spouse or the estate;

Plus

The qualifying child/ren (biological or legally adopted children under the age of 21) are eligible for the monthly pension until the age of 21. A pension to the surviving spouse equal to 60% of the deceased pensioner’s pension at retirement before commutation, including any subsequent increases;

Plus

A further pension of 30% (for one eligible child) or 40% (for two or more eligible children) of the deceased pensioner’s pension at retirement before commutation, including any subsequent increases, in respect of any eligible children.

If there is no spouse’s pension payable, the percentage in respect of a single eligible child is increased to 60% of the deceased pensioner’s pension at retirement before commutation, including any subsequent increases. For two or more eligible children, the total percentage is increased to 100% of the deceased pensioner’s pension at the time of retirement before commutation, including any subsequent increases.

If there are no spouse’s or children’s benefits payable, a benefit equal to the excess amount of the lump sum, as specified below, over the total benefits paid to the pensioner until the time of death is paid to the estate. The lump sum comprises the following:

- A lump sum of R3000;

Plus

The greater of the two following calculations:

i. Twice the annual pensionable salary at retirement, less the pension benefits received since retirement;

Or

ii. The annual pensionable salary at retirement plus 10% of the final average pensionable salary per year of pensionable service, less pension benefits already received.

Triennially, the Eskom Pension and Provident Fund (“EPPF”), as per the EPPF Fund Rules, requires you, our pensioner, to complete an Evidence of Survival (“EOS”). The purpose is to verify your existence and to further ensure that our records/data are up to date for us to continue to pay your pension.

How do I submit my EOS?

Your EOS can be submitted through one of the following options:

1. USSD

The EPPF has launched its Unstructured Supplementary Service Data (USSD) functionality as part of the new channels. This service allows you to use your mobile phone to submit your EOS. Utilising the USSD platform means that you do not have to fill in any forms, go to the police station or worry about your form reaching the Fund on time:

NOTE: Please follow the guide on the link below, should you require assistance:

2. Electronic Form (e-Form)

For those that have access to the member portal an e-form is available for direct update of your record. Follow the guidelines outlined in the guide on this link: EOS e-Form Guide. Please ensure that you are registered on our safe and secure member portal.

Pensioners who have not yet registered, please register here and follow the guidelines outlined in the getting started manual. Click here to access the manual.

To upload scanned copies of your EOS form on the member portal, please follow the guidelines by clicking here. Documents must be less than 5MB and in PDF.

3. Physical Evidence of Survival (EOS) Form

The option of physical Evidence of Survival (EOS) is still available.

To return the forms to the Fund, e-mail a copy of the form to webupdate@eppf.co.za

What happens if I don't submit my EOS form?

If the Fund does not receive your EOS by the payroll closing date, the payment of your pension will be suspended until the EPPF receives your form. The implications of not submitting on time can be far reaching e.g. aside from not receiving a pension, certain third party deductions may not be processed, e.g. medical aid payments etc.

Are widows; widowers and guardians with minor children required to submit an EOS?

Yes. Widows, widowers, and guardians with minor children in receipt of a pension, as well as disabled children in receipt of a lifelong pension, is required to submit an EOS. The following should be noted:

Pre-Retirement Counselling

All members exiting the Fund are required to meet with a Retirement Fund Consultant (RFC) six months before their exit. The purpose of the counselling is to assist and provide you with information needed to make an informed decision when retiring. The RFC will also guide you as to what is required in the completion of the Retirement application form.

Retirement application

The member with the help of Human Resources (HR) must complete the application form.

This application form is used to process the pension as per the member’s instruction.

If previously divorced, members are encouraged to submit their divorce documents to the Fund to prevent delays in processing as the divorce documents are to be reviewed by the Fund’s legal team.

Documents

All documents requested on the application form must be provided to the Fund before the member’s exit where the quality assurance pertaining to the documents can be completed. These can be provided electronically.

Last Contribution

The EPPF will wait for the final confirmation and the last contribution. The contributions are received from the employer by the 7th of the month after your retirement and once allocated. Thereafter, the applicable interest rates are loaded at which time the claim processing commences.

Calculation

The member’s final retirement calculation is done in accordance with the Fund rules.

Tax

The retirement calculation is sent to SARS to confirm the tax deductible on the benefit.

Cash lump sum

The member is paid the Nett cash lumpsum value if he/she has opted for that.

Monthly Pension

The arrear monthly pension is loaded along with any deductions as indicated by the member. Thereafter, the pension will run monthly by means of the EPPF’s payroll system.

Letter

The member is sent a welcome letter providing them with their monthly pension value and the tax certificate.

Pensioner Card

The card is produced and posted to members which enables them to get discounts, this could be store or region specific.

The Fund is notified of the death by a family member or via the monthly payroll which does an upload from the Department of Home Affairs.

The applicant needs to complete a Death Application form. This form provides information that the Fund requires to load the spouse and/or eligible children.

The applicant is to provide the Fund with the relevant supporting documents as indicated on the application.

The final pension value is calculated in accordance with the rules of the Fund.

The monthly pension values along with any deductions as indicated on the application is loaded.

The arrear monthly pension is paid. Thereafter the pension is run by means of the EPPF’s payroll system on a monthly basis.

A payment letter is sent to the beneficiary(ries) providing them with the details of their monthly pension.

A payslip is provided to each recipient of a pension on a monthly basis.

Please complete a Consent to Receive Email Payslips and Correspondence form which is available via the member portal. Once you have completed the form, please fax or post it back to the EPPF. Click here to log on to the member portal and access the form.

The spouse’s pension is payable for the duration of your lifetime, regardless of whether you remarry or not.

Depending on the investment performance of the EPPF, the Board of Trustees may declare a bonus which is payable in December of that year. Pensioners are advised in December of each year whether a bonus is payable through a newsflash.

There are various factors which contribute to your tax fluctuating:

In December there was a bonus paid so your tax deduction was different from other months;

In January there was a pension increase which also created a difference in tax payable;

In the February payroll medical aid contributions increased. Pensioners aged 65 years and older used to get a full medical aid rebate. However as medical aid contributions increase the taxable income decreases.

The new tax year begins in March. The Fund’s payroll system annualises tax based on the latest tax earnings and the last year’s tax tables. Since the Fund’s pension payroll runs in advance on the 1st of each month, new tax tables for the new tax year are always implemented in the April payroll. However, please note that the new tax tables implemented in April are implemented retrospectively to the March payroll as per tax changes announced in the budget speech. This means that your tax on the April payroll will include the March payroll deduction adjustments. Your tax should then stabilise from the May payroll onwards.

Section 18(2) of the Income Tax Act has been repealed. This means that pensioners who are 65 years and older are no longer granted the full medical aid rebate by the employer during the tax year. Instead they are granted the medical tax credits by the employer according to the number of dependants they have on their medical aid. The section of the Income Tax Act that deals with medical aid tax credits is section 6A of the Income Tax Act.

Medical aid medical aid expenses (such as medication, doctor’s consultations etc.) and tax credits in respect of expenses are granted during the assessment year of tax returns. Should it happen that the pensioner has paid too much tax due to medical expenses not being deductible by the employer; SARS will refund the excess to the pensioner.

Medical aid contributions and medical expenses are granted in terms of section 6B of the Income Tax Act.

The Medical Scheme Fees Tax Credit for individuals is a credit which applies in respect of contributions paid by the pensioner who has a taxable income up to the last day of the tax year to a registered medical scheme. The amount of credit is based on the following values per month in the year of assessment in respect of which the contributions were paid in respect of the pensioner, the pensioner’s spouse and any other dependants.

The employer’s contribution is not disclosed on the payslip but it is disclosed on the tax certificate under the deduction code 4493. The pensioner’s own medical aid contributions are disclosed under code 4005. Both of these amounts are added to form the total medical aid contributions, which is listed under code 4497, the medical aid tax credits are disclosed on code 4116, the medical aid expenses will be disclosed on code 4120 as a zero value since EPPF is not privy to pensioner’s expenses so the medical expenses credit will be granted by SARS.

SARS gets this information when the Fund submits the tax certificates on the pensioners’ behalf during the employer annual submission time.

For taxable income rates, rebates and tax thresholds applicable to individuals for each financial year, visit the South African Revenue Services’ website on www.sars.gov.za.

The Evidence of Survival (EOS) form is used by the EPPF to ascertain whether people in receipt of a pension from the EPPF, who live outside South Africa are still alive and are rightfully in receipt of a pension. EOS forms are sent out annually to pensioners living outside South Africa and pensioners have a few months in which to complete them from the date on which the form is sent to them.

The EPPF always advises pensioners of the opening and closing dates for EOS form submission. Should the EPPF not receive your form by the EOS submission closing date, your pension will be suspended until the form is received. Please contact the EPPF if you have not received an EOS form or Click here to log into your profile and download the form.

Yes, you are still obliged to submit your returns as a confirmation of the information submitted by the employer on your behalf. In your instance, the EPPF represents the employer as the provider of a monthly income.

An AA88 is a garnishee order issued to the employer (the EPPF) against you by SARS for monies owed by yourself to SARS. Monies owed are usually due to non-submission of tax returns and non-payment of tax owed. An AA88 was previously referred to as an IT88.

When the employer or the EPPF receives this garnishee order it is required by law to comply and deduct the amount owed to SARS from your pension and pay it over to SARS on your behalf. This might affect your other deductions, as a SARS garnishee order takes precedence over other deductions.

Please contact your nearest SARS office to resolve your outstanding tax issues. You can contact SARS on 0800 00 72 77.

To change your banking details when you relocate to another country, you must submit the following documentation to us:

Original, certified copy of your identity document or passport

An original, completed, International Banking Form (IBF). The IBF must be completed by the bank to which you want to transfer your benefit, or by your foreign exchange service provider.

Click here to log into your profile and download the IBF.

Remember to also advise us of your change in address. Click here to contact us in order to update your address and other contact information.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique.