Dear in-service member

We’ve put together this explainer to help you understand what the two-pot retirement system means while we continue with member engagement sessions, both online and in-person.

Much has been said in the media, and especially on social media, and this is what the two-pot retirement system means for you

Two-pot is a reference to how retirement savings will be separated to allow you access to a cash portion while preserving the remaining portion of those retirement savings. Your money will be put into different ‘pots’. These two pots are your Savings Component or ‘savings pot’, and your Retirement Component or ‘retirement pot’.

The legal process of implementing the two-pot retirement system

The most important point to remember is that the two-pot retirement system is still in proposal stage. It is not law yet. What has happened so far is that National Treasury and the South African Revenue Service (SARS) published updates to the proposed two-pot retirement system in June this year. The intention of National Treasury and SARS is that the two-pot retirement system will be effective from 1 March 2024.

The aim of the two-pot retirement system is to allow members early access to a portion of their retirement benefits while still in-service

The 2023 Draft Revenue Laws Amendment Bill as well as the 2023 Draft Revenue Administration and Pension Laws Amendment Bill include the following two main aims of the proposed two-pot retirement system:

- To allow you, as an in-service member, to access a portion of your retirement benefits while still employed; and

- To help you preserve the greater amount of your retirement benefits, so you have a monthly pension to support you once you retire.

There’s some misunderstanding around two-pot; mainly around how much can be accessed

What’s important to remember as an in-service member is that the proposed two-pot retirement system legislation only affects your future retirement benefits (made by you or on your behalf by your employer) after 1 March 2024. All the Fund benefits that you’ve accumulated up to 1 March 2024 are not affected by the proposed two-point retirement system legislation.

Your Fund benefits up to 1 March 2024 will be known as the Vested Component or ‘vested pot’. The dictionary definition of ‘vested’ in this scenario refers to the unconditional guarantee of your benefits. What this means in your case as an in-service member is that this Vested Component will still be accessible to you, under the current terms and conditions, should you change jobs. So, you’ll still be able to withdraw the full Vested Component amount should you change your job and you’ll only have to pay the applicable tax. Therefore, the rules that apply to your benefits up to 29 February 2024 will continue to apply to the vested pot into the future.

Retirement benefit contributions made after 1 March 2024

Contributions to retirement savings made after 1 March will be split into two parts. One third of pensionable service will go into one pot which will be the Savings Component. The other two thirds of retirement contributions will go into another pot which will be the Retirement Component.

For in-service EPPF members

The one important point to remember is that EPPF is a defined benefit fund, so your two pots will only be filled from each month of additional service that you accrue from 1 March 2024.

What’s likely in store for in-service members as EPPF prepares for 1 March 2024

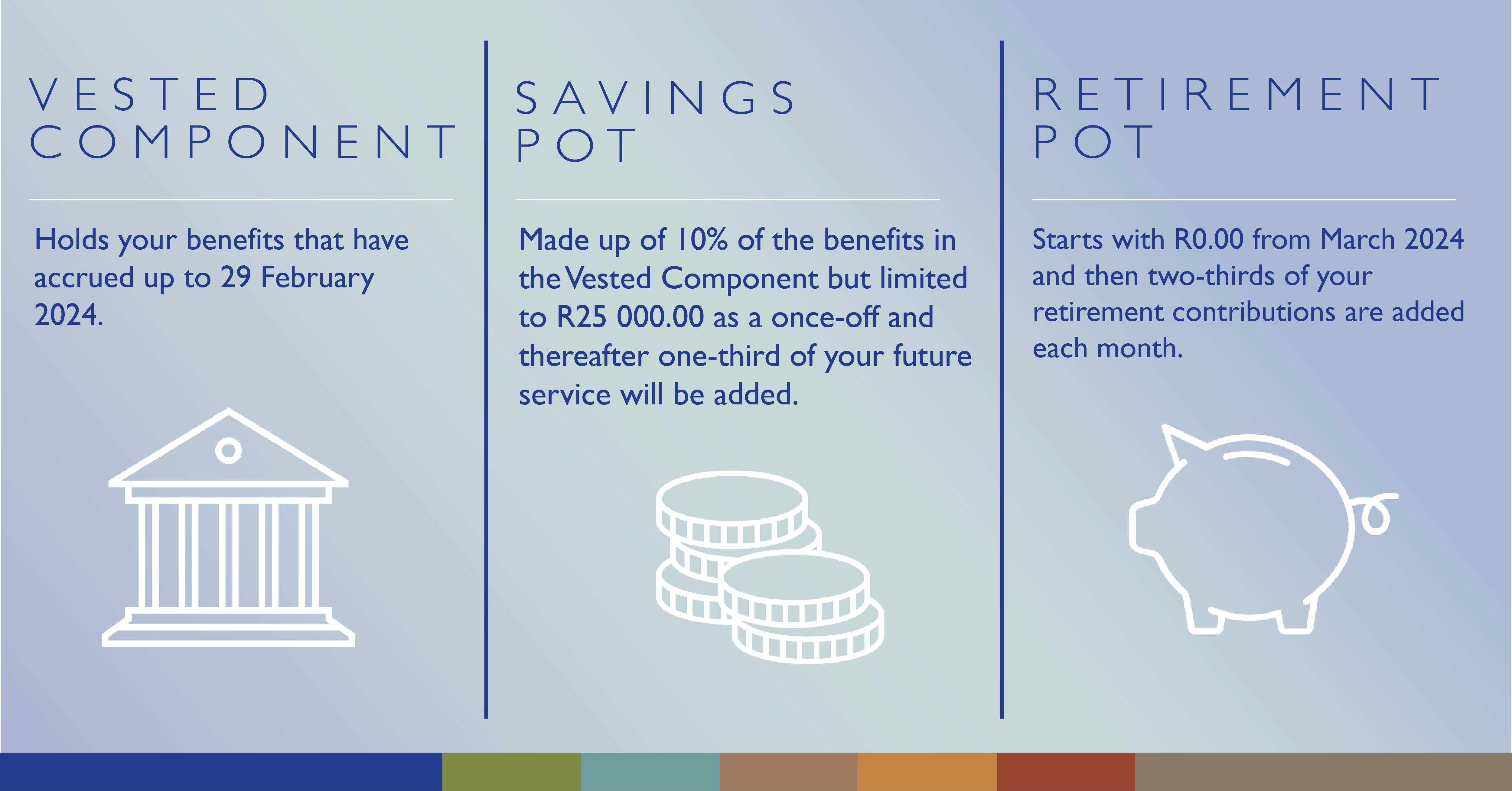

- On 1 March 2024, all in-service members will have a Vested Component (which will hold the in-service member’s benefits that have accrued up to 29 February 2024), a Savings Component (which will include 10% of the benefits in the Vested Component but will be limited to R25 000.00 as a once-off and thereafter one-third of the in-service member’s future service will be added), and a Retirement Component (which will start with nothing and then the in-service member’s two-thirds of service each month will be added).

- In-service members will be allowed to make one withdrawal per tax year from the Savings Component.

- This withdrawal from the Savings Component will not be allowed if a member has less than R2 000.00 in their Savings Component, and any withdrawal will be taxed as income at the in-service member’s marginal tax rate. The Fund will need to apply for a tax directive on behalf of the in-service member before the cash can be taken.

- No lump sum (cash) benefit may be taken from the Retirement Component when a member changes jobs.

- When changing jobs, a member may access a lump sum (cash) benefit from:

- the Savings Component if they did not take any withdrawal from that pot in that tax year. However, if they took a withdrawal from the Savings Component in that tax year, they can only take cash if the value is below R2 000.00. If they took a withdrawal and the value is R2 000.00 or more, then they may only transfer the Savings Component to their new employer’s fund; and

- the Vested Component as the rules applicable before 1 March 2024 will continue to apply to this pot.

- All accrued benefits in the Retirement Component will be locked in until retirement. When you retire, you will not be able to take any portion of your Retirement Component as a cash lump sum as this pot will be used to provide you with a pension at the date that you retire. This means that the Retirement Component cannot be accessed by an in-service member during their membership as it will provide a pension at retirement.

There’s no action required from you as an in-service member at this stage

It’s important that you manage your expectations as there’s a lot of misinformation and misunderstanding about what the two-pot retirement system will mean for individuals.

In terms of the usual passage of legislation, once public comments have been considered, National Treasury and SARS will engage stakeholders through public workshops to discuss and understand the feedback. There will then be parliamentary committee hearings and public hearings. Should Parliament pass the legislation, it will then go to the President to be signed into law (an Act of Parliament).

EPPF will continue to update you accordingly

The Fund will continue to send you regular communication when there’s an update that’s relevant to you. We will also have ongoing online and in-person member engagement sessions.

Kind regards

The EPPF Team