FUND PERFORMANCE TO 30 SEPTEMBER 2022

THE FUND’S ASSETS

The third quarter started well with asset prices rebounding but the positive sentiment was short-lived as monetary policymakers around the world are focused on controlling persistently high inflation. The assets of the Fund followed suit as asset prices continued to drop. As of 30 September 2022, the Fund’s assets are valued at R166.6 billion, down from R169.6 billion a quarter ago. The funding ratio, which is the ratio of assets divided by liabilities remains healthy and above 100%, approximately 152.05% (on a mark-to-mark basis) as of 30 September 2022, meaning that the Fund’s assets are more than sufficient to cover all the Fund’s liabilities. A strong funding ratio well above 100% indicates a sustainable Fund.

THE FUND’S RETURNS

FY23 followed on like FY22 ended with an elevated Consumer Price Index (CPI) benchmark due to accelerating inflation. Thus driving the Fund’s returns below their respective CPI linked benchmark return for the 1-year, 3-year, 5-year and 10-year periods. CPI came off a high of 7.8% year-on-year in July 2022 but moderated to 7.5% in September. Over a 10-year period to September 2022, which is most appropriate for a pension fund with long-dated liabilities, the Fund’s 10-year return of 8.83% marginally underperformed the absolute 10-year target of CPI + 4.5% (9.7% on a rolling basis). The rising inflation was driven by tight supply constraints and increasing food prices hurting price valuations of major asset classes.

In the past 12 months to September 2022, domestic Nominal bonds was the best performing asset class relative to benchmark, up 0.8%, followed by Inflation Linked bonds which is relatively up 0.1%. Domestic Listed equities performed in line with the benchmark, while Cash and Listed property underperformed their respective benchmarks by 0.6% and 0.1%, respectively.

Internationally, Africa listed equities excluding SA was the best performing asset class relative to benchmark, up 11.7%, followed by China's onshore equities which is relatively up 2.9%, emerging markets equities relatively up 0.2%. International property and Africa bonds performed in line with their benchmark while International developed listed equities underperformed its benchmark by 1.7%.

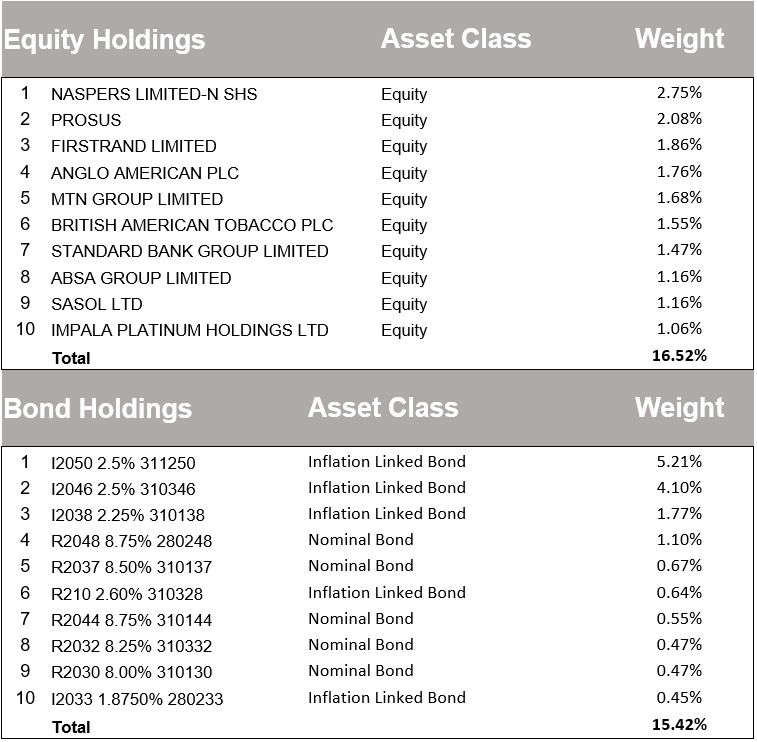

THE FUND’S TOP EQUITY AND BOND POSITIONS (30 September 2022)

THE FUND’S APPOINTMENTS AND UNLISTED INVESTMENTS FOR QUARTER 3, CALENDAR YEAR 2022

The Fund approved an investment of USD 60 million commitment of the unlisted Africa debt allocation towards Ninety-One’s Sustainable Africa Credit Opportunity (SACO) Fund. The investment is subject to successful contractual negotiations, compliance with all regulations and getting the appropriate licensing and the EPPF to not being more than 25% of Ninety One’s SACO fund.

There were no new manager appointments in quarter two.

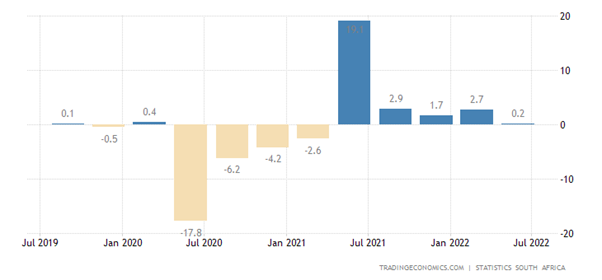

ECONOMIC GROWTH

After two consecutive quarters of positive growth, real gross domestic product (GDP) decreased by 0,7% in the second quarter of 2022 (Q2: 2022). The devastating floods in KwaZulu-Natal and load shedding contributed to the decline, weakening an already fragile national economy that had just recovered to pre-pandemic levels. The flooding hurt seven of the ten industries, most notably agriculture and manufacturing, which are down by 7.7% and 5.9%, respectively. Transport, finance and personal services were the only industries recording a positive growth of 2.4%, 2.4% and 0.1% in the second quarter, respectively. Annual GDP increased by 0.2% in the second quarter of 2022 following an expansion of 2.7% in the first quarter of 2022. A loss of trading hours due to load shedding, flooding and foot-and-mouth disease all weighed negatively on the economic outlook.

South African Annual GDP Rate (%)

INFLATION AND INTEREST RATES

Inflation accelerated in the third quarter, recording 7.8% year-on-year in July, and has come off that high, down 7.6% in August and further 7.5% in September. It remains to be seen if inflation has peaked as this will dictate the rate and size of monetary policy intervention by the SARB. 2022 has recorded aggressive rate hikes, with the latest being 0.75% in September 2022 following another 0.75% in July 2022. The repo rate is now at 6.25% in September 2022 and is expected to rise further locally and in other markets, to curb runaway inflation.

South African Inflation Rate (%)

EQUITIES AND CURRENCY

South African Capped SWIX equities

Capped SWIX lost 2.43% on a total return basis in the third quarter to September 2022, with underlying sector performance was disparate, reflecting a combination of high earnings expectations, lower commodity prices, higher bond yields. Consumer Discretionary (-2.91%), Materials (-2.95%), Financials (-4.1%), Real Estate (-3.91%) and Communication Services (-6.22%) were the notable laggards, together contributing a total of 2.91% to negative performance. Precious metals and mining benefited from a staggered rebound in gold and platinum prices during the quarter. Telco’s (10.44%) and Consumer staples also managed to outperform the market in the same period due M&A news flows.

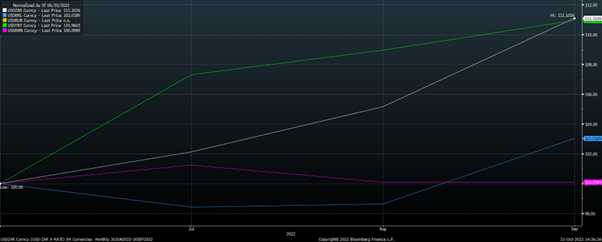

South African Rand against the US Dollar

The rand lost 11.1% in the third quarter to September 2022 against the US dollar. Cyclical headwinds, such as lower commodity prices, have been amplified by structural constraints, such as load shedding and political uncertainty. While the trade balance should remain in surplus in 2H22, there are notable downside risks amid loadshedding and transportation disruptions. The weaker rand has contributed to the market pricing in a more aggressive monetary policy response by the SARB. USD/ZAR was trading above 16.09 by end of the third quarter to September 2022.

GLOBAL MARKETS

The third quarter started on a positive note with a rebound in equities amid hopes of a dovish pivot from the Fed. The upbeat sentiment lasted well into August but was stamped out by a crisp hawkish message from Fed Chair Powell at Jackson Hole. The US Federal Reserve hiked its policy interest rate in the third quarter twice by 0.75% to 3.25% by September 2022. Liquidity tightening amid a strong US dollar and QT is keeping the SARB on the front foot to ensure that real rate differentials do not go against the rand. While the MPC does not target the rand directly, they are cognisant of the potential inflation risk posed by excessive rand weakness. As such, the short-term evolution of monetary policy will very much remain a function of what the Fed does.

Russia’s war in Ukraine continues to impair production and trade of a wide range of energy, food and other commodities. The supply of energy to the Euro Area is limited as winter approaches, placing immense strain on households, businesses and governments. With rapid inflation and monetary policy normalization, the United States may also experience slower economic growth. While China’s recovery from the Covid19 lockdowns has strengthened, economic growth is expected to remain below longer term trends.

CONCLUSION

Tactically, the Fund still looks to increase its offshore exposure gradually as the rand is expected to weaken and South African assets are expected to underperform global assets due to tightening financial conditions and declining appetite for riskier assets.

Strategically, from the perspective of changing the Fund’s strategic asset allocation to incorporate the new offshore limit, the Fund is in the process of finilising its annual robust asset and liability modelling exercise, which focuses on the long term, in sympathy with the Fund’s liability duration, to inform its decision making.

The SARB still sees a gradual rate hike path through 2023, given its current inflation forecasts. Economic and financial conditions are expected to remain more volatile for the foreseeable future. In this uncertain environment, monetary policy decisions will continue to be data dependent and sensitive to the balance of risks to the outlook. The MPC will seek to look through temporary price shocks and focus on potential second round effects and the risks of de-anchoring inflation expectations. The Bank will continue to closely monitor funding markets for stress.